Virtually hidden among the more controversial provisions of the Tax Cut and Jobs Act adopted late last year, Opportunity Zones, which are intended to promote economic activity in lower-income areas by giving preferential tax treatment to investors, are starting to attract attention from both the financial industry and the public interest sector. This program allows capital gains invested in qualified funds (“Opportunity Funds”) to be deferred until the earlier of the disposition of the fund or December 31, 2026, when the program ends. Further, the amount of gain taxed on disposition of the fund is reduced by 10% if held at least 5 years (15% if held at least 7 years)—and on top of that, if the fund is held at least 10 years, its tax basis is stepped up to its fair market value at the time of disposition, thus exempting all gain from tax!

Virtually hidden among the more controversial provisions of the Tax Cut and Jobs Act adopted late last year, Opportunity Zones, which are intended to promote economic activity in lower-income areas by giving preferential tax treatment to investors, are starting to attract attention from both the financial industry and the public interest sector. This program allows capital gains invested in qualified funds (“Opportunity Funds”) to be deferred until the earlier of the disposition of the fund or December 31, 2026, when the program ends. Further, the amount of gain taxed on disposition of the fund is reduced by 10% if held at least 5 years (15% if held at least 7 years)—and on top of that, if the fund is held at least 10 years, its tax basis is stepped up to its fair market value at the time of disposition, thus exempting all gain from tax!

While estimates vary, this program is expected to attract at least $10 billion in investment each year during the term of this program, in which Opportunity Funds must invest at least 90% of their capital into a broad range of assets that must be located within Opportunity Zones (eligible low-income areas chosen by each state’s governor and selected by the Treasury Department). One type of investment that will likely see a challenge arising from this program is Section 1031 exchanges, as real estate investors may find the greater asset flexibility, streamlined procedures, and potential for full avoidance of capital gains to be an attractive alternative. It will be critical for real estate investors to carefully evaluate the pros and cons of these tax-advantaged investments to determine which is most suitable for their individual situations.

Last month, the IRS issued proposed regulations to provide guidance regarding the implementation of this tax incentive arrangement. These proposed rules, along with a Revenue Ruling published at the same time as these proposed rules, clarify a number of the specific provisions of this new law. While a detailed description of these rules is beyond the scope of this article, by way of example, only capital gains or gains treated as capital gain (such as Section 1231 gains from the sale of real property) are eligible for deferral. As such, ordinary income recapture arising from the sale of depreciable person property does not qualify for this treatment. Although these proposed rules become effective only after they are issued in final, taxpayers may rely on them if they do so in their entirety and consistently.

Unlike previous attempts by Congress to use tax incentives to lure capital into impoverished areas, this effort could attract more money due to its lack of bureaucratic and funding restrictions and broad asset range, according to Rebecca Lester of Stanford’s Graduate School of Business. One of her concerns, however, is whether this program will actually provide a benefit to those who currently live in these areas, or simply enrich its investors and produce gentrification of these areas. Professor Lester is currently in the process of evaluating the impact of these inducements, and has already published a preliminary analysis of this new law, summarizing its main terms, offering selected information on the actual Opportunity Zones chosen for this program, setting forth potential concerns for the future of the program, and making recommendations for various reporting requirements to help understand whether this program is satisfying its goals.

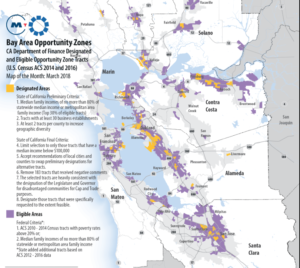

For those of you who are interested in understanding how this program may relate to our local economy, a map of the Opportunity Zones located in the San Francisco Bay Area can be found here. It will be very interesting to see how these tax incentives affect the investment environment across the country in these economically disadvantaged areas as this program gets underway.